Formula Debugging Techniques#

While the Refinery formula system catches syntax and type errors automatically, the most challenging debugging scenarios involve semantic issues - formulas that are syntactically correct but produce unexpected or wrong results. This guide focuses on systematic approaches to diagnose and fix these semantic problems.

Table of Contents#

Common Semantic Issues#

- The formula works but the results are wrong.

Here are the most frequent semantic problems:

Data Alignment Issues - Series with different frequencies or date ranges

Missing Data Propagation - Holes in data becoming NaNs when series combine

TZ-Aware vs TZ-Naive Incompatibility - Cannot mix timestamped and date-based series

Time Shifting for Business Periods - Business days don’t align with calendar boundaries

Circular Dependencies - Formulas depending on each other creating loops

Deep Formula Performance - Complex formulas becoming slow or hard to debug

Progressive Debugging Strategy#

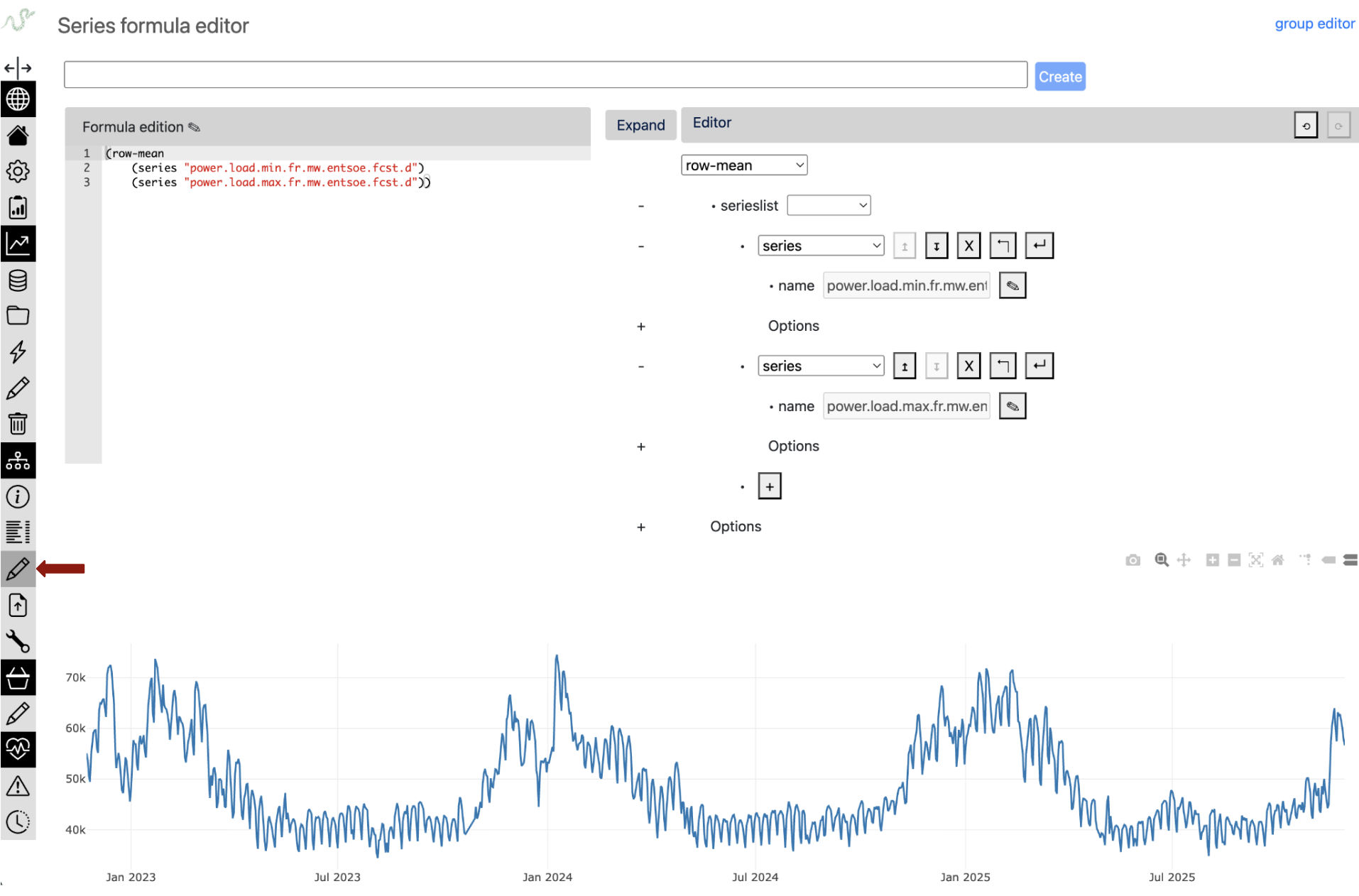

Using the Formula Editor#

The formula editor is your primary tool for incremental formula construction and debugging. It provides real-time validation, immediate visual feedback, and powerful debugging capabilities that make semantic issue detection much easier.

Key Capabilities:

Dual Editor Interface

The formula editor provides both a text editor with ACE editor integration for code-based formula editing and a visual tree editor for graphical formula construction. Changes in either editor automatically update the other in real-time, allowing you to choose the interface that best fits your workflow while maintaining perfect synchronization between both views.

Real-time Formula Evaluation

Formulas are automatically evaluated 2 seconds after your last edit, with results plotted immediately as you type. Syntax and evaluation errors are highlighted inline using ACE editor annotations, while loading states provide visual feedback during formula evaluation. This creates an immediate feedback loop that accelerates the debugging process.

Interactive Formula Building

You can build complex formulas incrementally, with each change immediately reflected in the plot visualization. The tree editor provides structured formula building with context-aware editing assistance, while real-time syntax checking and type validation catch errors as you work.

Advanced Editor Features

The editor includes full undo/redo history tracking for both text and tree editors, allowing you to experiment freely and revert changes when needed. You can save and update formulas directly from the editor, with separate modes for series and group formula types. Protected formulas can be viewed in read-only mode for reference without modification risk.

Incremental Building Workflow in the formula editor:

;; Example: Building a complex financial indicator step by step

;; Step 1: Start with basic data access (plot immediately visible)

(series "close_price")

;; Step 2: Add simple transformation (see the shift effect)

(time-shifted (series "close_price") #:days -1)

;; Step 3: Calculate returns (observe the scale change)

(div (sub (series "close_price")

(time-shifted (series "close_price") #:days -1))

(time-shifted (series "close_price") #:days -1))

;; Step 4: Add smoothing (see noise reduction)

(rolling (div (sub (series "close_price")

(time-shifted (series "close_price") #:days -1))

(time-shifted (series "close_price") #:days -1)) 5)

;; Step 5: Final indicator with parameters you can adjust live

(rolling (div (sub (series "close_price")

(time-shifted (series "close_price") #:days -1))

(time-shifted (series "close_price") #:days -1)) 20)

Visual Debugging Benefits:

- Immediate Pattern Recognition

Spot frequency mismatches by observing plot density

Detect missing data gaps visually

Identify outliers and anomalies in real-time

See aggregation effects on data distribution

- Temporal Alignment Verification

Overlay multiple series to check alignment

Zoom into specific periods to verify time shifts

Visual confirmation of resampling effects

Holiday/weekend gap analysis

- Scale and Range Validation

Immediate feedback on value ranges

Detect unit conversion issues

Spot normalization problems

Verify percentage vs ratio calculations

Common Debugging Patterns in the formula editor:

;; Pattern 1: Missing data investigation

(series "sensor_data") ;; See the gaps

(series "sensor_data" #:fill "ffill") ;; See fill effect immediately

;; Pattern 2: Aggregation verification

(resample (series "hourly_data") "D") ;; Check daily aggregation visually

(resample (series "hourly_data") "D" #:method "sum") ;; Compare sum vs mean

;; Pattern 3: Rolling operation tuning

(rolling (series "noisy_signal") 5) ;; Too little smoothing?

(rolling (series "noisy_signal") 20) ;; Better smoothing

(rolling (series "noisy_signal") 50) ;; Too much smoothing?

Inspect Intermediate Results with python#

# Check data properties at each step

def debug_series(series, name):

print(f"\n=== {name} ===")

print(f"Length: {len(series)}")

print(f"Date range: {series.index.min()} to {series.index.max()}")

print(f"Frequency: {series.index.freq}")

print(f"NaN count: {series.isna().sum()}")

print(f"Value range: {series.min():.4f} to {series.max():.4f}")

print(f"Sample values:\n{series.head()}")

# Apply to each step

returns = tsa.eval_formula('(series "daily_returns")')

debug_series(returns, "Daily Returns")

rolling_mean = tsa.eval_formula('(rolling (series "daily_returns") 252 #:method "mean")')

debug_series(rolling_mean, "252-day Rolling Mean")

Data Alignment Problems#

Series with Different Frequencies#

Problem: Combining daily and monthly data without proper alignment.

# ❌ PROBLEM: This will cause unexpected results

problematic_formula = '(add (series "daily_sales") (series "monthly_budget"))'

# The monthly budget gets broadcast/aligned in unpredictable ways

result = tsa.eval_formula(problematic_formula)

# Result: Data loss - operation succeeds but produces meaningless results

Debugging approach:

# Inspect the frequency mismatch

daily_sales = tsa.eval_formula('(series "daily_sales")')

monthly_budget = tsa.eval_formula('(series "monthly_budget")')

print(f"Daily sales frequency: {daily_sales.index.freq}")

print(f"Monthly budget frequency: {monthly_budget.index.freq}")

print(f"Daily sales length: {len(daily_sales)}")

print(f"Monthly budget length: {len(monthly_budget)}")

Solutions:

;; Solution: Aggregate daily to monthly (downsampling)

(add (resample (series "daily_sales") "M" #:method "sum")

(series "monthly_budget"))

;; Downsampling is reliable - aggregation works within known boundaries

;; ❌ Solution 3: NEVER DO THIS - Calendar approximation is dangerous!

(add (series "daily_sales")

(div (series "monthly_budget") 30)) ;; Calendars are tricky: NEVER APPROXIMATE THEM!

;; This fails because months have different lengths (28-31 days)

;; February gets wrong allocation, leap years break it, etc.

;; ALWAYS use calendar-preserving operations like resample!

Different Date Ranges#

Problem: Series covering different time periods.

# Debugging date range mismatches

discontinued = tsa.eval_formula('(series "bloomberg_prices")') # 2010-2023, stopped feeding

current = tsa.eval_formula('(series "reuters_prices")') # 2022-2024, actively updated

print(f"Discontinued source: {discontinued.index.min()} to {discontinued.index.max()}")

print(f"Current source: {current.index.min()} to {current.index.max()}")

print(f"Overlap period: {max(discontinued.index.min(), current.index.min())} to {min(discontinued.index.max(), current.index.max())}")

Solution:

;; Use priority to create seamless time series

;; Old source first, then newer source patches/extends it

(priority (series "bloomberg_prices") (series "reuters_prices"))

Date Range Slicing for Optimization#

Slicing can optimize data retrieval and avoid unnecessary overlap:

;; Efficient source combination: use Reuters only after Bloomberg ends

;; This minimizes database queries by avoiding the 2022-2023 overlap

(priority

(series "bloomberg_prices")

(slice (series "reuters_prices") #:fromdate "2023-01-01"))

;; Result: Bloomberg data through 2022, Reuters from 2023 onwards

;; Avoids fetching overlapping data from both sources

Missing Data Propagation#

Understanding Holes propagation#

Problem: Holes in upstream data are propagated when series are combined.

# Reality: "Holes" (missing timestamps) are the main issue, not stored NaNs

sensor_a = tsa.eval_formula('(series "sensor_a")') # Has data Mon-Fri

sensor_b = tsa.eval_formula('(series "sensor_b")') # Has data every day

# When combined, holes in sensor_a become holes in the result

combined = tsa.eval_formula('(add (series "sensor_a") (series "sensor_b"))')

print(f"Sensor A points: {len(sensor_a)}") # e.g., 250 (weekdays only)

print(f"Sensor B points: {len(sensor_b)}") # e.g., 365 (every day)

print(f"Combined points: {len(combined)}") # 250 points

# Note: Some operations can create holes:

# - div by zero, log of negative values, rolling std with insufficient data

# But the main challenge is managing holes in upstream series

Solutions:

;; Use fill options strategically

(add (series "a" #:fill "ffill") (series "b" #:fill "ffill"))

;; Use priority for fallback

(priority (add (series "a") (series "b"))

(series "backup_calculation"))

;; Control aggregation NaN handling

(row-mean (series "sensor_1") (series "sensor_2") #:skipna #t)

Date and Time Semantic Errors#

TZ-Aware vs TZ-Naive: A Fundamental Distinction#

Context: The Refinery uses two types of series for different purposes:

TZ-aware series: Timestamped measurements (sensors, market data) - stored in UTC

TZ-naive series: Period-based reference values (regulatory limits, accounting data)

Problem: Comparing real-time measurements against daily regulatory thresholds.

# Real scenario: pollution monitoring vs regulatory limits

no2_readings = tsa.eval_formula('(series "no2_sensor_readings")') # TZ-aware (µg/m³ every hour)

daily_limit = tsa.eval_formula('(series "no2_regulatory_limit")') # TZ-naive (daily threshold)

print(f"Sensor readings tz: {no2_readings.index.tz}") # UTC

print(f"Regulatory limit tz: {daily_limit.index.tz}") # None - just dates

# This fails - cannot compare timestamped data with date-based limits

try:

exceedances = tsa.eval_formula(

'(sub (series "no2_sensor_readings")

(series "no2_regulatory_limit"))')

except TypeError as e:

print("Cannot mix tz-aware and tz-naive series!")

# The semantic question: which timezone should define "a day" for the limit?

Solutions:

;; Solution 1: Convert sensor data to naive

;; This interprets "a day" according to local calendar

(sub (naive (series "no2_sensor_readings") "Europe/Paris")

(series "no2_regulatory_limit"))

;; Solution 2: Aggregate hourly data to daily before comparison

;; This preserves tz-awareness but creates daily averages

(sub (resample (series "no2_sensor_readings") "D" #:method "mean")

(tzaware (series "no2_regulatory_limit") "Europe/Paris"))

;; The choice depends on regulatory interpretation:

;; - Option 1: Local calendar days

;; - Option 2: 24-hour periods in consistent time reference

Time Shifting for Business Period Alignment#

Problem: Business periods often don’t align with calendar boundaries.

;; Example: Gas day runs 06:00 to 06:00

;; Hourly gas flow data needs alignment to calendar days

;; Raw hourly data

(series "gas_flow_m3h")

;; 2024-01-15 00:00 belongs to gas day 2024-01-14!

;; 2024-01-15 06:00 belongs to gas day 2024-01-15

;; Shift by -6 hours to align gas day with calendar day

(time-shifted (series "gas_flow_m3h") #:hours -6)

;; Now 2024-01-15 00:00 contains flow from 06:00

;; Perfect for daily aggregation by calendar day

Formula Dependencies and Recursion#

Deep Formula Performance#

Problem: Deeply nested formulas can be slow and hard to debug.

# Check formula depth

depth = tsa.formula_depth('complex_formula')

if depth > 20:

print(f"Warning: depth {depth} may impact performance")

# For debugging, test at different expansion levels

for level in [5, 10, 15]:

partial = tsa.formula('complex_formula', level=level)

result = tsa.eval_formula(partial)

print(f"Level {level}: OK" if result is not None else f"Level {level}: Failed")

Debugging approach:

Deep formulas are naturally composed of many simpler formulas, each doing one job well. Use /tsinfo interface to navigate the dependency tree and spot where problems occur (typically bad values or data holes at specific formula levels).

Performance Optimization

For formulas with performance issues, the Refinery provides a caching system that can materialize intermediate results. See Formulas: when to use a cache/materialized view for details on setting up cached series.

Using TSInfo Interface for Formula Analysis

For a deep formula:

Navigate to the series via the catalog search

Check the inline plot visualization - toggle “inferred freq” to see data holes as points

Review the Statistics panel for data quality metrics

Use the Cache tab to see cache status and policies

Enable “History mode” to compare revisions and debug temporal issues

Use the formula depth selector to examine different expansion levels

Understanding the Reactive System#

The Refinery implements functional reactive programming where formulas are pure functions computed lazily on demand. Understanding this helps debug unexpected behavior.

Key Properties:

1. Lazy Evaluation

Updates store data but don’t trigger computation:

# Update primary series

tsa.update('gas_injection_facility_001', new_data, 'operator')

# Data is stored, but no formulas compute yet

# Get a formula that depends on this data

result = tsa.get('eu_energy_balance_optimized')

# NOW the entire dependency graph computes

# (assuming eu_energy_balance_optimized uses gas_injection_facility_001)

2. Time-Dependent Behavior

Formulas appear pure but get() results can change:

result1 = tsa.get('deep_formula')

tsa.update('base_series', new_data, 'operator')

result2 = tsa.get('deep_formula')

# result1 != result2 (underlying data changed)

# But see point 4 - historical data eventually becomes immutable

3. The “Today” Operator

The (today) operator returns: - Current date when called without revision_date - The revision_date when provided

;; Formula taking last 30 days

(rolling (slice (series "data")

#:fromdate (shifted (today) #:days -30)) 7)

This creates a moving window that follows either wall-clock time or revision time.

4. Eventual Purity

Historical data becomes immutable once “settled”:

# For audit date 2023-12-31, if no more data can be inserted before it:

year_end = tsa.get('financial_metric', revision_date='2023-12-31')

# This result is now permanent - perfect for compliance